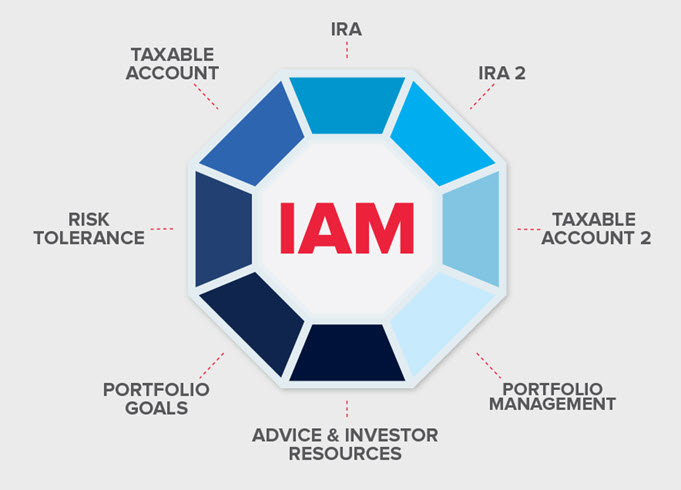

We have officially released Investment Account Manager v4.0…

We have officially released Investment Account Manager v4.0 in its current form so customers can begin using it immediately. Continue reading We have officially released Investment Account Manager v4.0…

Posted on March 14, 2026

2025 Year End Tax Planning Tips

As the close of 2025 quickly approaches, investors should start thinking ahead, reviewing and taking advantage of tax saving strategies. Here are three important tips that will help investors manage tax consequences, while helping to better manage their investment portfolio(s). Continue reading 2025 Year End Tax Planning Tips

Posted on October 16, 2025

Concentrated Investment Positions

With the recent run-up of stock market levels over the past several years, many investors might find one or more of their investment holdings have appreciated considerably in value, now representing a disproportionate percentage of the total portfolio value. Investors must pay attention to these concentrated investment positions. While different measurements can define a concentrated Continue reading Concentrated Investment Positions

Posted on September 17, 2025

Unified Investment Account Management

Unified investment account management is extraordinarily important in order to achieve investment success. Continue reading Unified Investment Account Management

Posted on August 5, 2025

2025 Mid Year Portfolio Rebalancing Tips

As we’ve reached the mid point of 2025, we pass along this reminder that now might be an ideal time to review your portfolio and identify if any rebalancing changes may be necessary to reach long-term goals. Here’s a multi-step guideline that you will find helpful to accomplish this important portfolio management task. Continue reading 2025 Mid Year Portfolio Rebalancing Tips

Posted on June 2, 2025

Avoiding Investing Pitfalls

Even the most experienced of investors, including professional advisors, occasionally overlook the fundamentals of investing, often resulting in negative consequences for their portfolios, and investing clients. For less experienced investors, the challenges to avoid these same factors can be even more difficult and can lead to far greater disappointing results. Continue reading Avoiding Investing Pitfalls

Posted on April 15, 2025

2025 Understand and Manage your Risk Tolerance

Make 2025 the year you learn to understand and manage your risk tolerance. The beginning of a new year is an ideal time to evaluate your investment portfolio. Make time to first review your long-term goals, which can be anything from finally tackling debt or building your emergency fund to stashing away money for Continue reading 2025 Understand and Manage your Risk Tolerance

Posted on March 1, 2025

Planning for Retirement: 10 Axioms for Effective Investing

What’s the key to making good investment choices? It isn’t necessary to understand the inner workings of the securities markets or the mathematical economies underlying investment theory. Instead, 10 axioms of effective investing provide the critical cornerstone for guiding investment philosophy and making decisions. This will ensure that you meet the universal goal of creating Continue reading Planning for Retirement: 10 Axioms for Effective Investing

Posted on February 1, 2025

Reviewing and Understanding your Investment Objectives

With the start of 2025, now is an ideal time for investors to review their forward-looking investment objectives, understanding these objectives are affected by short- and long-term needs and changing requirements. This fact sheet provided by the CFA Institute will help you work with your financial adviser to determine how to best meet your financial Continue reading Reviewing and Understanding your Investment Objectives

Posted on January 1, 2025

2024 Year End Portfolio Management and Tax Planning

One important benefit of using a portfolio management and investment record keeping system is the ability to utilize and access information for improved year-end decision making, including useful tax planning, monitoring and reporting tools. This includes lot-by-lot accounting, since in most cases, investment portfolios will consist of multiple assets, acquired at varying times, with different Continue reading 2024 Year End Portfolio Management and Tax Planning

Posted on December 4, 2024